Music R'lyeh, this is Eric with low VA rates, wearing my red shirt as always. As we always do, fighting! What you guys can see is the crew that's here with me, they're all in red. That's what we do here. As a reminder, we wear red on Fridays, and red stands for "Remembering Everyone Deployed." Even if you're not deployed, you may have family members that are in the military. This is kind of an outward expression of supporting the troops wherever they are. So, with that said, today we're going to talk about whether or not VA loans have PMI. Okay, PMI stands for private mortgage insurance. Okay, I'm just gonna put "mortgage insurance" here for those that are tuning in. The real question here is: Do VA loans have mortgage insurance? Okay, the answer is no. I can turn off the camera right now, and you guys would have learned something today, but I want to educate everyone that's watching. Hopefully, we'll get some questions, so be thinking. We're really hoping that these live videos start garnering more questions. Even if you just leave them and can't stand listening to me talk for the next three or four minutes, you can type them in and leave them, and we can answer them later. But, that said, VA loans do not have mortgage insurance. What VA loans do have, however, is something called a VA funding fee. Okay, I do not have the best writing in the world, but conventional loans, okay? That's what most civilians get. If you didn't serve in the military, you cannot get a VA loan. With a conventional loan, you either have to put 20% down when you're buying your home, so if you're going to buy a $200,000 home, you have to have $40,000...

Award-winning PDF software

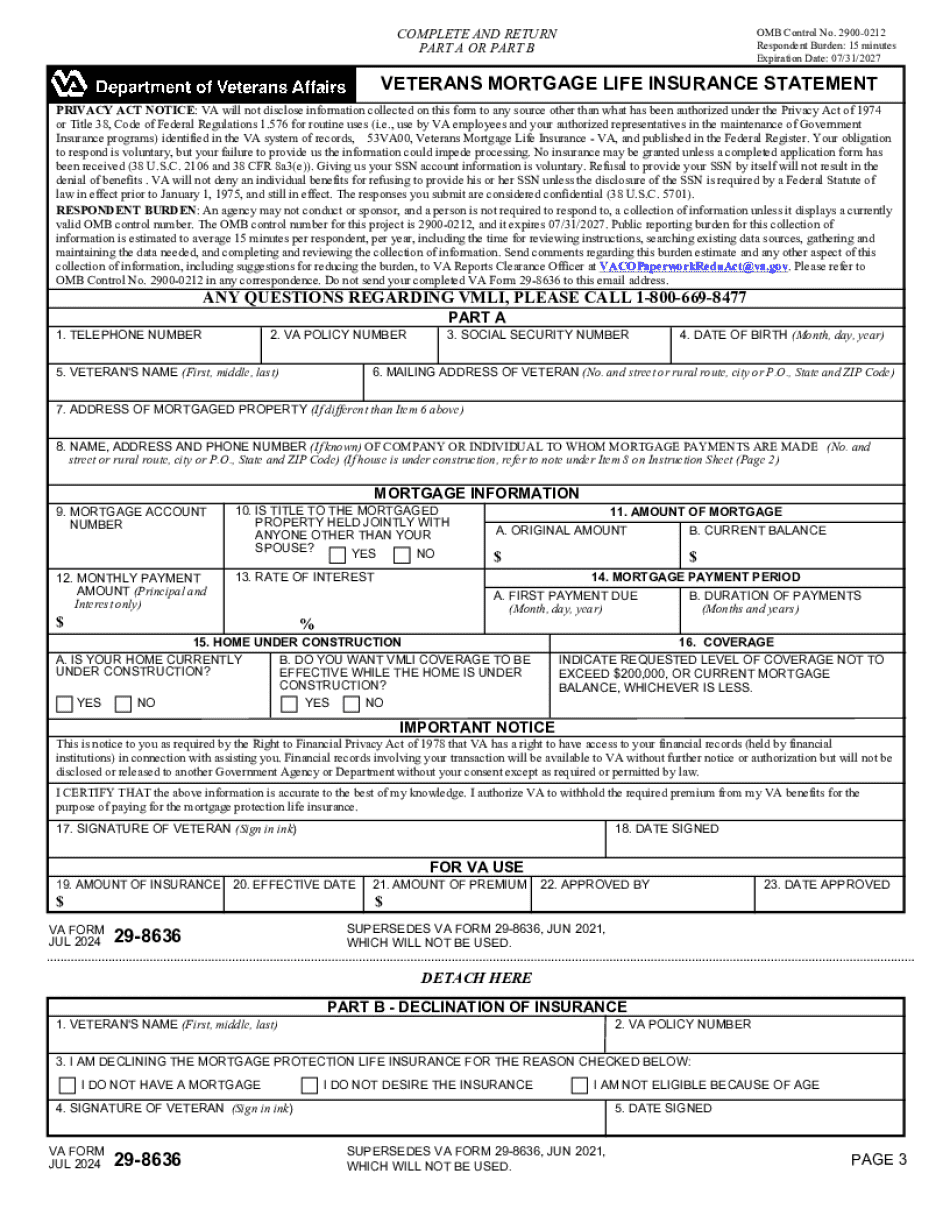

Va loan mortgage insurance calculator Form: What You Should Know

The benefit is that you can qualify for a VA loan mortgage without having a down payment of any kind. Vermont Life Insurance Companies: Vermont-Affiliated Life Insurance Co 8 days ago — Vermonters-Affiliated Life Insurance Companies offers a portfolio of life insurance products and business that are tailored to the Military.com Premium Service Nov 10, 2025 — It's time to get your mortgage rate estimate! Our premium service provides the most accurate mortgage loan rate estimates. It includes all essential information about your mortgage loan, including the mortgage rate itself, the principal amount, the monthly payments, the loan terms, the appraisal and a complete listing of your mortgage options for a total peace of mind and the peace of mind of all the other people on the military premium service. Military, Veterans and Retired Military — How To Read a VA Mortgage Loan 6 days ago — An easy way to tell if your VA loan is a good one — if your appraiser is happy with the price. The easiest way, of course, is the appraiser's report. But how do you know what that look is? You are going to need to do a little digging online! Military, Veterans and Retired Military — How To Read a VA Mortgage Loan | Military.com 6 days ago — To get a rough value on a VA loan — the VA loan calculator will give you a quick estimate of the monthly mortgage payment. Once you're done, click the loan calculator that you've created on Army.com to compare your VA payments with your FHA and conventional mortgage payments, and see what you might qualify for… Military, Veterans and Retired Military — How To Read a VA Mortgage Loan | Military.com 6 days ago — The military, as an organization, works to support and elevate the health and well-being of its members worldwide. The military's mission is to defend the nation, provide a safe, secure and quality environment for military families and service members. Military, Veterans and Retired Military — How To Read a VA Mortgage Loan | Military.com 5 days ago — For those who have been approved for a VA loan (by VA), the loan paperwork looks very similar to the standard mortgage, but there are a few minor changes that you are going to see.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Va 29-8636, steer clear of blunders along with furnish it in a timely manner:

How to complete any Va 29-8636 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Va 29-8636 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Va 29-8636 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Va loan mortgage insurance calculator