Award-winning PDF software

Va life insurance loan Form: What You Should Know

APPLY- CATION : S-DVI DEPARTMENT OF VETERANS AFFAIRS SECURITY. PROCLAMATION. S-DVI provides up to 10,000 of life insurance for eligible veterans. APPLY- CATION : S-DVI DEPARTMENT OF VETERANS AFFAIRS SECURITY. PROCLAMATION. S-DVI provides up to 10,000 of life insurance for eligible veterans. DEPARTMENT OF VETERANS AFFAIRS Security. PROCLAMATION. SAVE THE DATE. S-DVI offers life insurance to eligible Veterans and their dependents (and their estates) for an estimated maximum of 10,000 per event depending on eligibility and service-related disability. S-DVI offers life insurance benefits through S-DVI Life Insurance Company, which administers the S-DVI's disability death benefits through its subsidiary, the Division of Veterans and Dependents Benefits. For inquiries concerning S-DVI, please call in Washington, D.C. or call in Texas. For additional information regarding the S-DVI, visit or call the company at. S-DVI offers coverage to eligible survivors of those whose life was insured by S-DVI on the life plan. The policies cover disability death benefits or death benefits equal to at least 10,000 per death. The S-DVI insurance policy terminates at age 45 for service-connected deaths (other than accidental deaths while suspected of suffering from a service-connected disability and other deaths that would occur under circumstances to which S-DVI's policy provided coverage), and at age 58 for service-connected deaths from service-connected and accidental causes, and at age 64 for other service-connected deaths. If an S-DVI beneficiary dies before age 64, S-DVI's insurance provide the remaining premium payment. The minimum age is 25 years. S-DVI, a division of The United States Department of the Treasury, has its office in San Francisco, California. S-DVI, Inc.

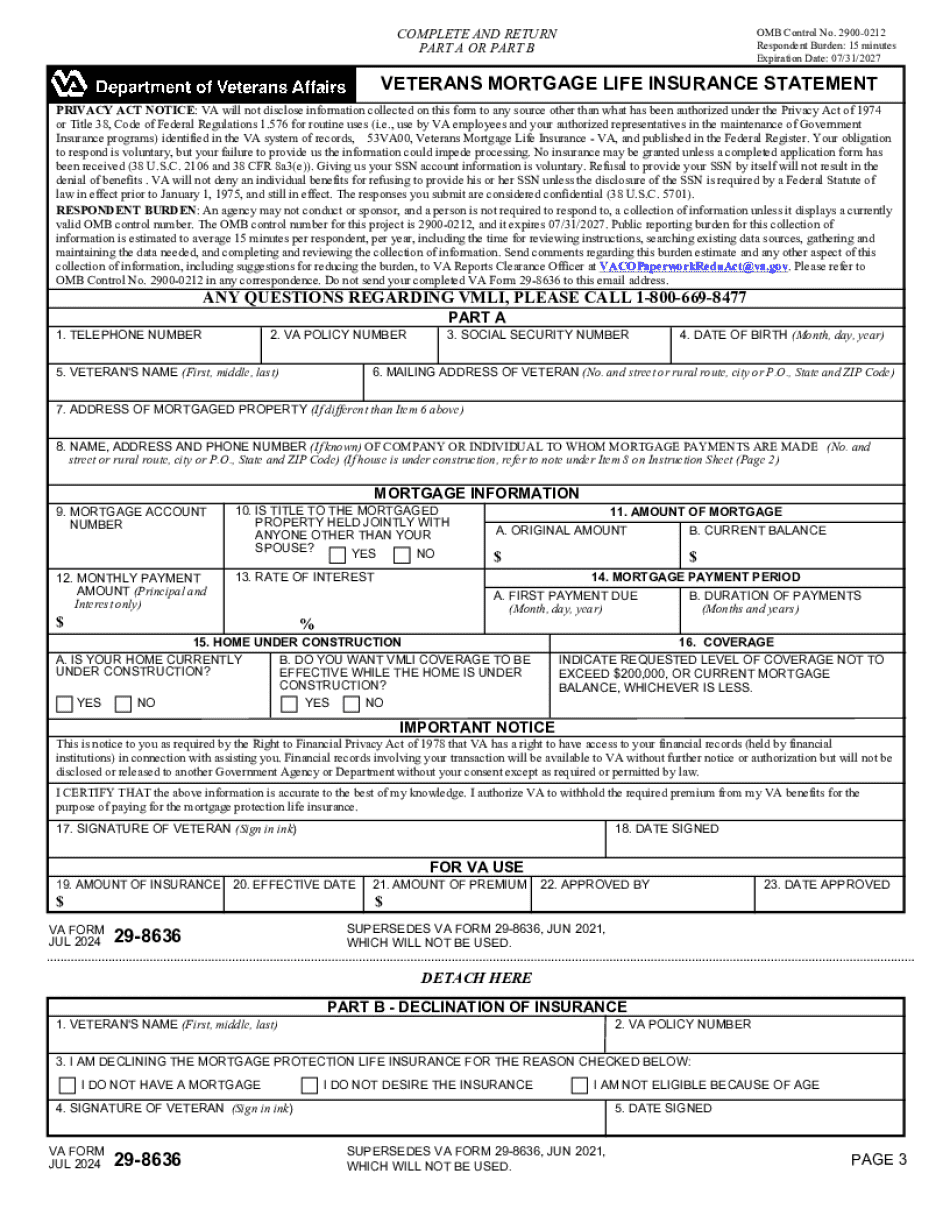

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Va 29-8636, steer clear of blunders along with furnish it in a timely manner:

How to complete any Va 29-8636 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Va 29-8636 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Va 29-8636 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.