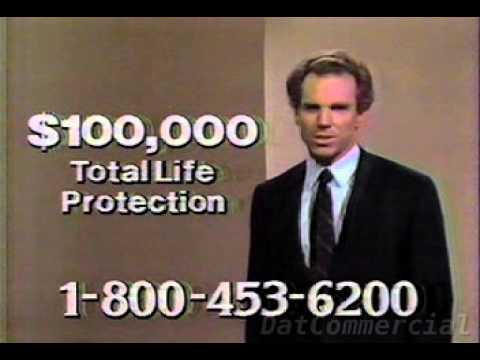

The following announcement is for honorably discharged US veterans, aged 18 to 59. The toll-free number shown on your screen is used to respond to the following. Do not repeat, do not miss this important information exclusively for veterans, veterans of all branches of service, and spouses of qualified veterans. Stand by for complete details. Already over two million veterans have called to find out how this card can serve them exclusively. Hi, I'm Roger Staubach. If you're a veteran aged 18 to 59 or the spouse or widow of a vet, write down this toll-free number because one quick phone call can bring you all the facts about a plan that offers you a choice of $10,000, $20,000, up to $50,000 in term life benefits. $50,000 for under $10 a month. And since your spouse is also eligible, your total family protection can reach up to $100,000. All this at affordable veterans rates. All you have to do is pick up the phone and call. Operators are ready now to serve you. In a matter of days, an information package will be sent directly to your home. In it, you'll find all you need to apply right away. In fact, you don't even have to take a medical exam. You'll also receive your own veterans life guard embossed with your name. It's all absolutely free with no obligation. As a veteran, you owe it to yourself to get the facts about this exclusive offer, so call now. Veterans, call 1-800-453-6200. That's 1-800-453-6200. An information package will be mailed to you immediately. Call now. You will also receive an updated guide to veterans benefits, showing what government benefits veterans are entitled to and how to collect. Operators are standing by. Call 1-800-453-6200. The information is free, and so is the...

Award-winning PDF software

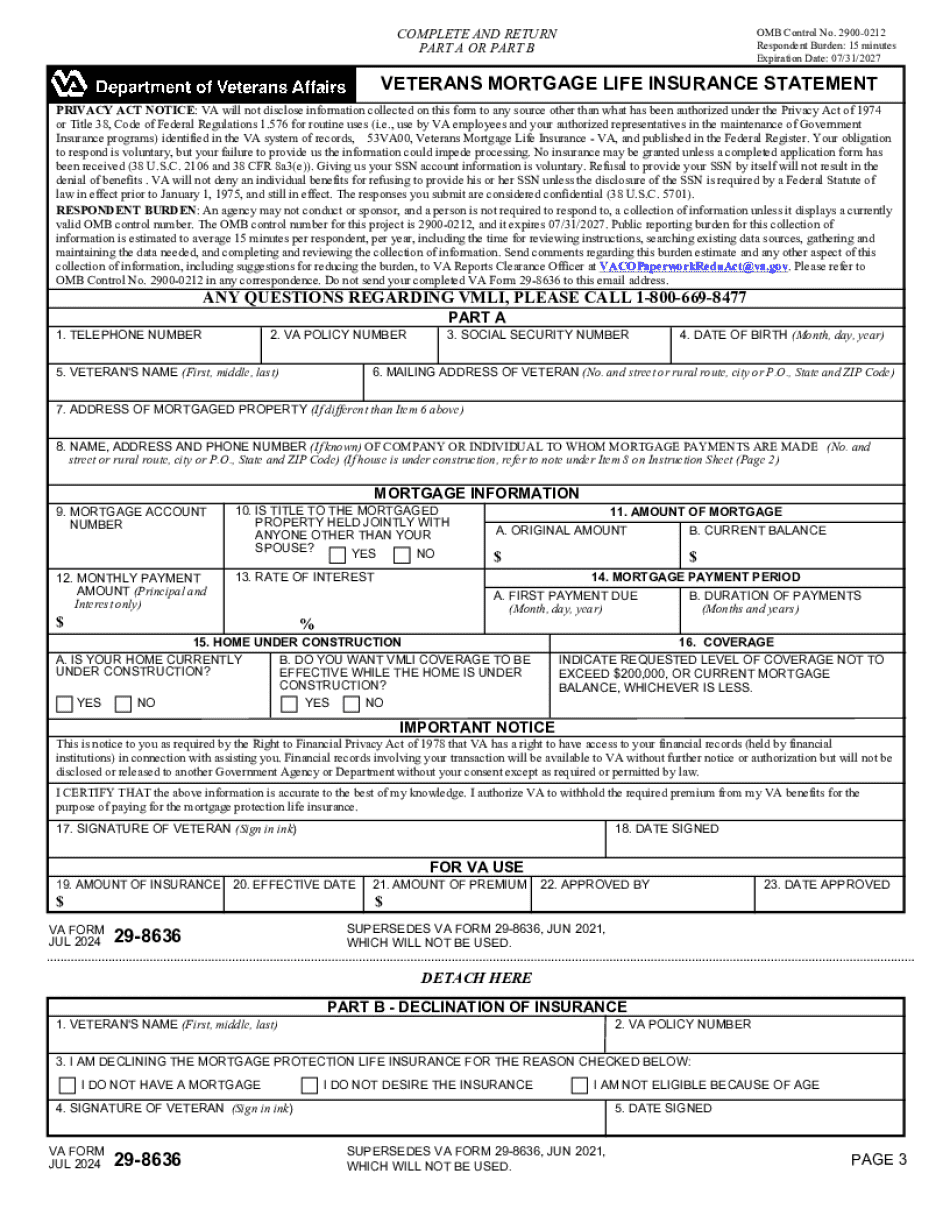

Va life insurance Form: What You Should Know

Please note that if you are not the owner of the policy, it is considered yours to have and dispose of in the same manner as any other policy. When a policy is surrendered for cash, the VA will contact the policyholder to provide the surrender value as provided on this form. This form will be on file within 3 business days of receipt of the surrender. When the surrender value reaches the VA, they will process a new claim and begin to collect any applicable amounts. When a policy is surrendered for a lump sum payments or the Cash Surrender Value or Policy Loan repayment amount is less than 1,000, the VA will process a new claim and begin to collect any applicable amounts. Once the refund amount has been received from the VA, the policy will be retired and the old policy will be retired. If, after 30 days of possession, the VA or its representatives determine that the surrender value is more than 1,000, the policy will be surrendered within 90 days. If the surrender value is more than 1,000, the policy will be surrendered by the owner. All refunds are processed within 90 days from when the policy was surrendered. Policy surrender value will be assessed as follows: Policy must be presented for presentation at the time of surrender. Policy must be surrendered in person at the following: You may have the surrender value assessed to you by anyone claiming to represent the U.S. Government and no physical evidence or paperwork must be provided. The sum will be assessed based on the amount in cash, the length of time the policy has been surrendered, the amount of payments made on the policy and the total Cash Surrender Value. The Cash Surrender Value will be assessed based on the amount in cash and will be subject to the tax laws of the state in which the policy is surrendered and where the policyholder lives. If the cash value equals or exceeds 4,000, the policy will be forfeit by the policyholder. The amount will be subject to state sales tax. The maximum surrender value that can be used at any time is 4,000. If the cash value is less than 4,000, the policy will be forfeit by the policyholder. The amount will be subject to state sales tax.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Va 29-8636, steer clear of blunders along with furnish it in a timely manner:

How to complete any Va 29-8636 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Va 29-8636 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Va 29-8636 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Va life insurance