Congratulations, you're officially a homeowner. Now, you get the joy of all the extra costs and benefits associated with owning your own house. As you're going through all the paperwork with your banker, you're asked if you want to purchase mortgage life insurance on your house. Puzzled, you're not sure. You've heard of term life insurance, but what is mortgage life insurance? Hey, this is Jeff Rose, a certified financial planner. A couple of years ago, I was asked the exact same question by a client who was buying their first house. They were asked if they wanted to purchase mortgage life insurance. At the time, I wasn't really sure what mortgage life insurance was. I had term life insurance on myself and my spouse, but what's this mortgage life insurance? Typically, when you buy life insurance, you do so to protect the income if something happened to you. So, if I were to pass away, I want to make sure I have enough life insurance to take care of my spouse and all our debt, including our mortgage. So, when I think of buying mortgage life insurance, I'm thinking I'll buy term, right? Actually, the answer is no. Mortgage life insurance is typically a product that is sold directly from the bank, and you're buying it directly to take care of the house. As you continue to make payments on your home or mortgage, the amount of life insurance declines or reduces over time. However, here's the big kicker: the beneficiary is not your spouse or kids, it's the bank or mortgage company. If something happens to you, the insurance payout goes directly to the bank to pay off your mortgage. Now, it sounds like a pretty good deal, I guess. Do I have a declining death benefit amount? Yes, because you're paying...

Award-winning PDF software

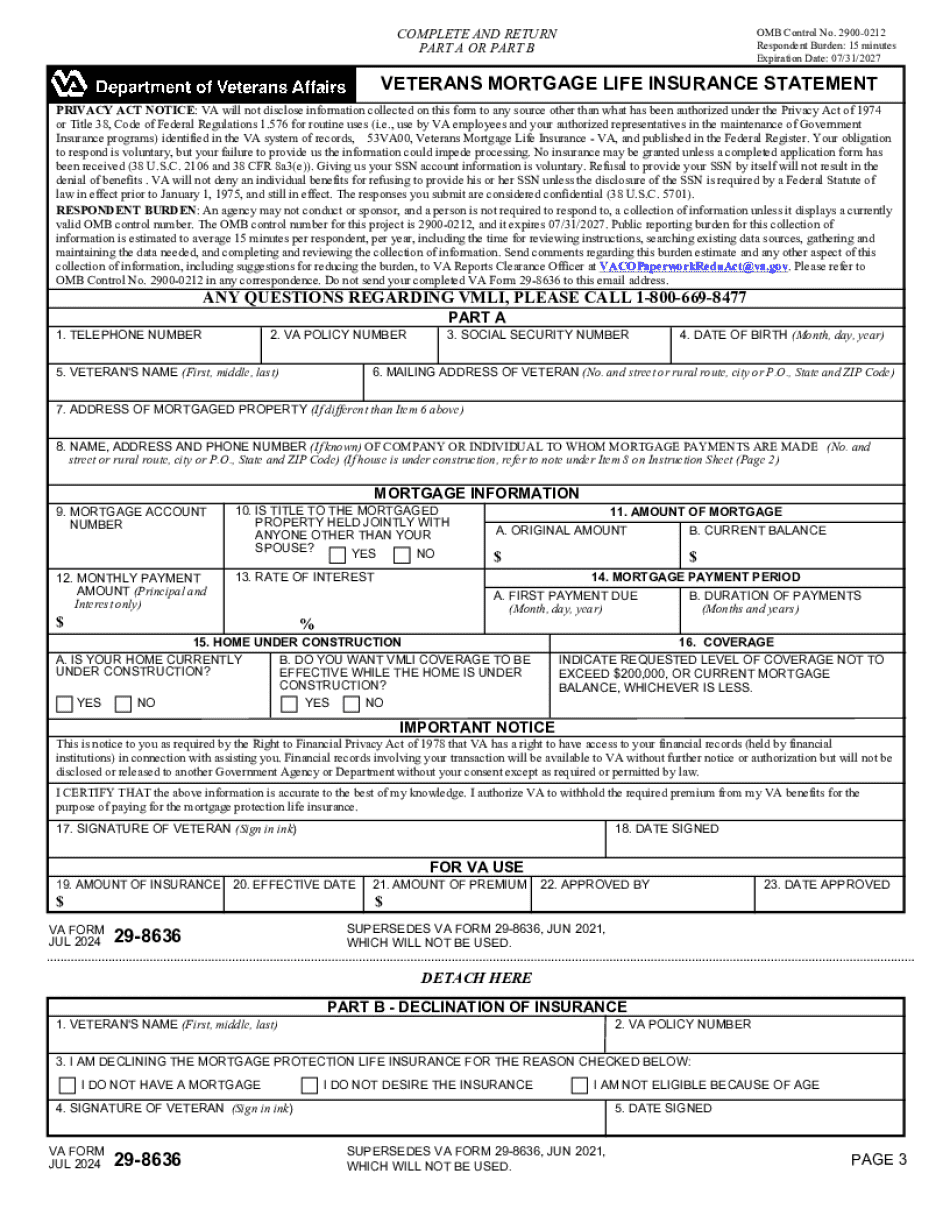

Veterans' mortgage life insurance Form: What You Should Know

Where do I submit Veterans Mortgage Life Insurance (MLI) by mail? You can submit a copy of the letter from Veteran Service Officers from an outside agency for Veterans to sign, OR you can submit a V.O.T. — (Veteran's Insurance Tracing Service) request form from the Veteran Service Officer at your station. When are the first installments due? When you complete the form, the date should be shown.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Va 29-8636, steer clear of blunders along with furnish it in a timely manner:

How to complete any Va 29-8636 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Va 29-8636 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Va 29-8636 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Veterans' mortgage life insurance