Hi, this is Dave Boy Key from Retirement Resources. Again, thanks for joining us. We're going to talk today about life insurance, specifically the cost of life insurance and how companies calculate that. Most life insurance is based on a cost per unit of coverage. For instance, $1000. So, what does it cost me to buy one thousand dollars of coverage? If I should die, my family or my beneficiary would receive that one thousand dollars. Well, it's based specifically on my age. The younger I am, theoretically, the longer I can pay that premium because I'm going to live longer. That's called mortality. The older an individual is, the less time they have to pay insurance premiums. So, therefore, the company has got to charge them more money for that same thousand dollar benefit. So, insurance companies price their insurance policies based on a unit, usually of a thousand, and it ranges based on whether an individual is younger or older. So, it's based on age. It's also based on whether they're male or female. Females tend to live historically a little longer than men, so the premiums are usually a little bit less for them at the same age as an individual. Again, the other thing they take into consideration is our health. A young person, specifically a young female, that doesn't have any health issues can get a very favorably priced policy, obviously compared to say, a gentleman age 75 who has multiple health issues. The premium is going to be much higher. So, folks, I suggest that you find a trusted financial advisor that specializes in life insurance. Sit down and have a talk with them. Find out how much it could cost you to get the coverage you need. You may be pleasantly surprised that it's...

Award-winning PDF software

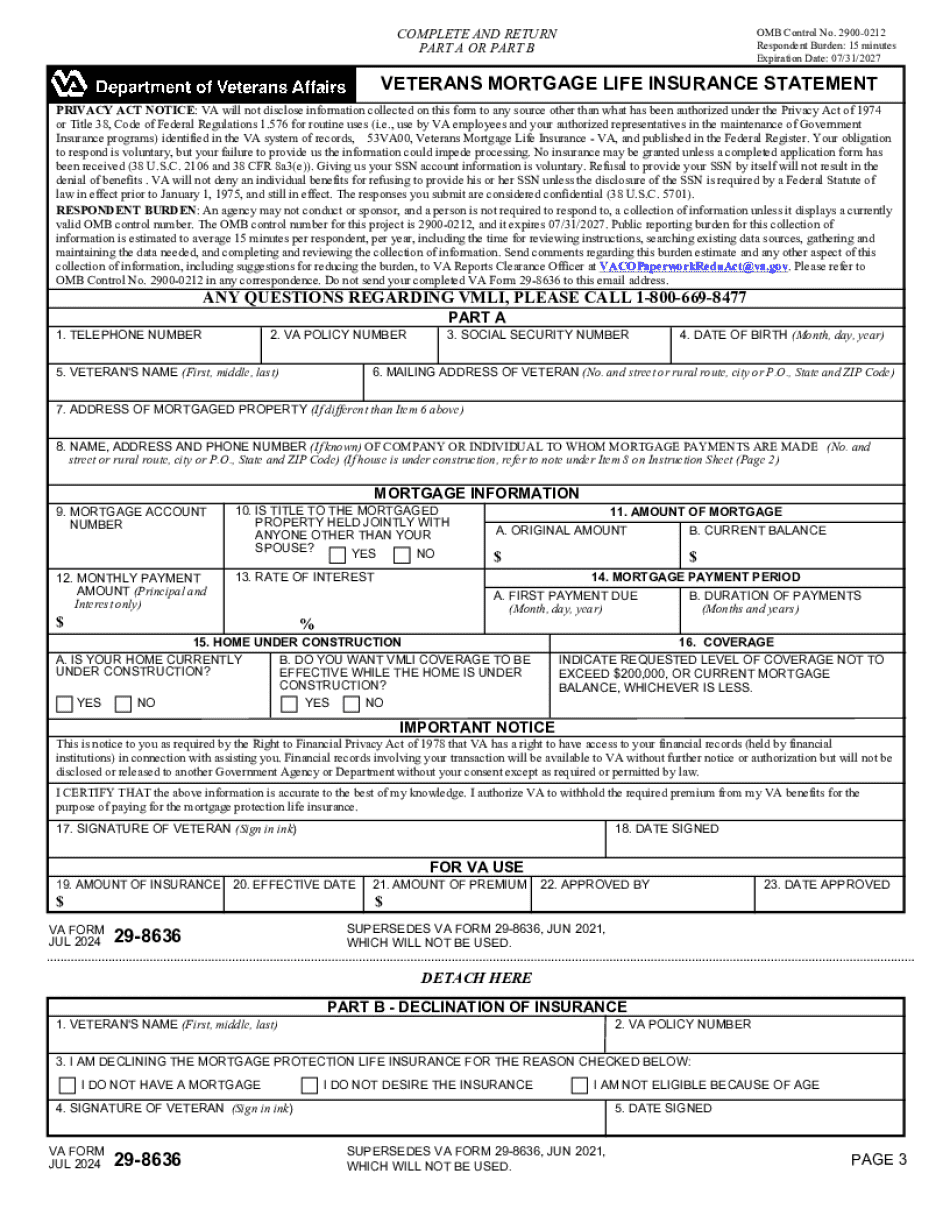

Va life insurance calculator Form: What You Should Know

Day of the year or anniversary of first disability after joining your employer's group plan. Retirement Benefits Calculator. Select coverage type and value on the right-hand side of the screen, and click 'Calculate'. Life Insurance Calculator. Choose Life Insurance policy coverage from the drop-down menu below.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Va 29-8636, steer clear of blunders along with furnish it in a timely manner:

How to complete any Va 29-8636 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Va 29-8636 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Va 29-8636 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Va life insurance calculator