Alright, okay, so let's start from the back to the beginning. Let's talk about time payment of claims. You've already discussed that, but let's go over it again. Remember, they have to pay us immediately upon receiving proof of loss. I went over that with you guys, letting you know that the test question may ask you how quickly the insurance company has to pay a claim after they get the proof of loss. The answer could be immediate, and that would be correct. But remember, as we get into this, you got it, you have to give them at least 60 days. So you can't file a lawsuit against them because they haven't paid yet. Until 60 days goes by. So immediate is probably correct when you see it, but the more accurate answer would be they got 60, they have 60 days to make the payment. Disability benefits have to be paid at least monthly. Disability benefits can be paid weekly and twice a month, but they can't pay them quarterly, semi-annually, and annually. Payment of claimants to payment of claims, those traditional policies we talked about, the reimbursement policies. Remember, we file a claim and the insurance company sends the money to the insured. But if the insured dies before the money gets there, then it's going to go to the beneficiary that the person would have named. And if there's no beneficiary, then it goes to the estate of the insured. But I didn't make that too clear, so I want to make sure it's clear to you. It doesn't go to the estate of the beneficiary. If the beneficiary dies and the insured is dead, it's going to go to the estate of the insured. Physical exams and autopsies, I mentioned to you. Okay, if...

Award-winning PDF software

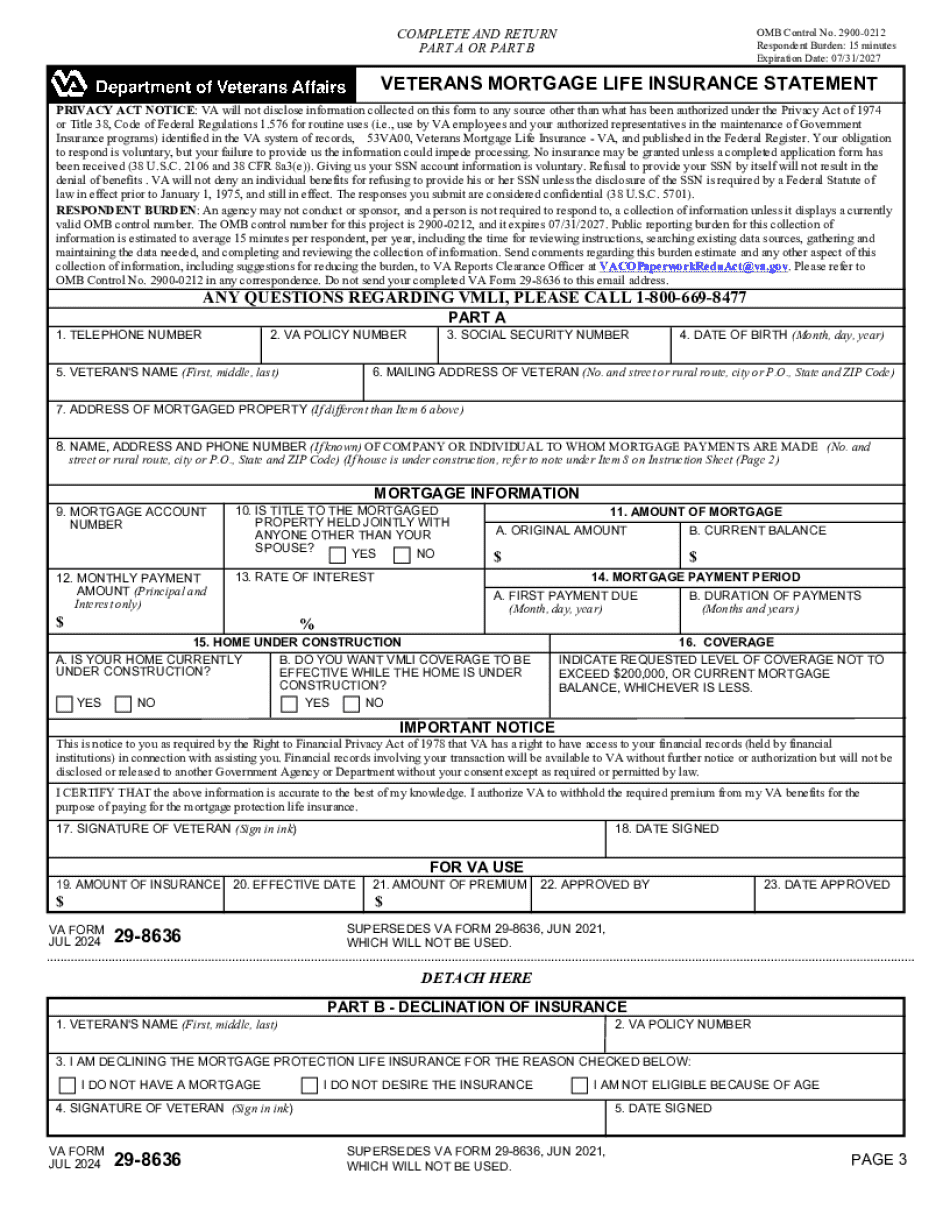

Va life insurance Form: What You Should Know

The Secretary of Veterans Affairs has directed us to dispose of retired military life insurance. If a veteran is age 55 or older and the policy has at least 25 years remaining after expiration date, VA is providing the policy owner with a cash surrender value in the amount of 200,000 and the beneficiary will receive a cash surrender value of 200,000. Veterans with one or more prior service-connected disabilities must request the surrender value of the life insurance policy, by completing this VA-provided form. If the policy or an associated death benefit already exists, the request must include the amount and/or benefits owed to that person. The surrender value may be paid within seven (7) business days. The surrender value is based upon a hypothetical scenario, whereby the life insurance policy owner lives to at least age 100 and at least 10 years have been paid on the cash surrender value and the spouse has retired at least 10 years. Veterans are not required to receive the surrender value, but if they wish to, they may do so. If applicable, the surrender value may be used to reduce the taxable value of the life insurance policy for up to two (2) years and may be used to reduce or defer the tax liability on the cash surrender value. Please reference 28 C.F.R. § 36.102(k) for more details. Form 29-1546, Request for Cash Surrender Value Vietnam-era Veteran Receivable Insurance Vietnam-era veteran receivable insurance is a life and annuity policy for eligible veterans. Veterans may have to surrender a policy to meet the required age requirements specified in the policy (generally 57 or older), or to satisfy an Income Tax requirement. The insurance will include a cash surrender value of 25,000. If the policy is surrendered before the age of 65, the surrender value can be used to reduce or defer the tax liability. If a policy was lost during World War II, a request for surrender value (see above) or death benefit(s) should be filed to the appropriate U.S. Department of Defense Financial Operations Center (DOC) for transfer. Please note that the current DFC process for Vietnam-era veteran receivable insurance includes two methods of payment: a cash surrender value and a death benefit if deemed necessary.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Va 29-8636, steer clear of blunders along with furnish it in a timely manner:

How to complete any Va 29-8636 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Va 29-8636 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Va 29-8636 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Va life insurance form